This story is part of slack help deskCNET’s coverage of how to make smart money move in an uncertain economy.

A strange twist on the story: Economic eventsThe US Treasury’s government saving bonds have been one of the most important investments in today’s world. Series 1 savings bondsIt has been particularly strong in recent months, reaching a record high 9.62% in the past six-months.

The interest rate for I bonds changes every six months and Tuesdays. Treasury announcedNew rate: 6.89%. This is lower than what you paid in bonds over the past two periods but it is still higher than the interest on it High yield savings accountsOr certificates of deposit.

How do I make the bonds? What interest rate do they pay? Who can buy them. Learn about Series 1 savings bond to see if it is a safe investment for you in times of uncertainty.

Learn more about inflation and investments How to invest during a bear marketAnd the Steps to take if you’re worried about stagnation.

What are Class I savings bonds and how do they work?

Savings bonds were introduced during the Great Depression in 1935 to provide a way for Americans to save money while also raising money for their federal government.

The US Treasury has added and has since halted production of several series of savings bonds—most notably Series E defense bonds, which helped fund the effort in World War II and continued long afterward. Today, there are only two series of savings bonds left: Series I and Series EE.

Series I bonds have variable rates that are linked to current inflation data. This means that the interest rate may change every six month depending on whether consumer price rises or falls. EE Series bonds are linked to long-term Treasury interest rate and will at least double their value in 20 years.

Original price was paper bondsLike large checks, most I bond can be sold electronically via the TreasuryDirect site. You can also still buy paper bonds—which currently feature portraits of famous Americans like Helen Keeler, Martin Luther King Jr., and Albert Einstein—with tax refunds.

How can I make bonds?

I Bonds can also be purchased electronically starting at $25 You can purchase paper bonds in denominations of $25, $50, $75, $100 or $200.

You can purchase I-bonds up to $10,000 electronically and $5,000 in paper bonds each year if you use money from your tax refund.

I Bonds are the best choice for those looking for a low-risk, long-term savings vehicle. Your bonds cannot be redeemed before the end of 12 months. There is also a three-month interest penalty if you redeem them before five years. Your I bonds can earn interest up to 30 year.

You won’t receive interest on I bonds or need to pay taxes on that interest until it’s cashed—although you can pay taxes each year on the earnings as you go. If you are using files I am obligated to pay for higher educationInterest may not be subject to any taxes.

How much will the bonds cost?

The I bonds’ interest rate has been 9.62% for the past six-months, which is the highest yielding savings bond since its introduction in 1998. The new I Bond’s inflation rate of 6.89% will continue through May 1, 2023.

The interest rates are what determine how much you can make from your savings. I bonds calculate interest ratesCombining a fixed rate that is the same throughout the bond holding with a six-month variable rate Consumer Price Index for all urban consumersCPI-U (which includes food and energy prices) is the CPI-U. The variable rate is subject to change twice a year, in the first days between May and November.

The flat rate for I bonds was 3.40% when they were introduced in September 1998. However, the days of decent fixed rates ended with 2008’s recession. Rates have been lower than 1% ever since. Since May 2020, I bonds have had a fixed rate of 0%.

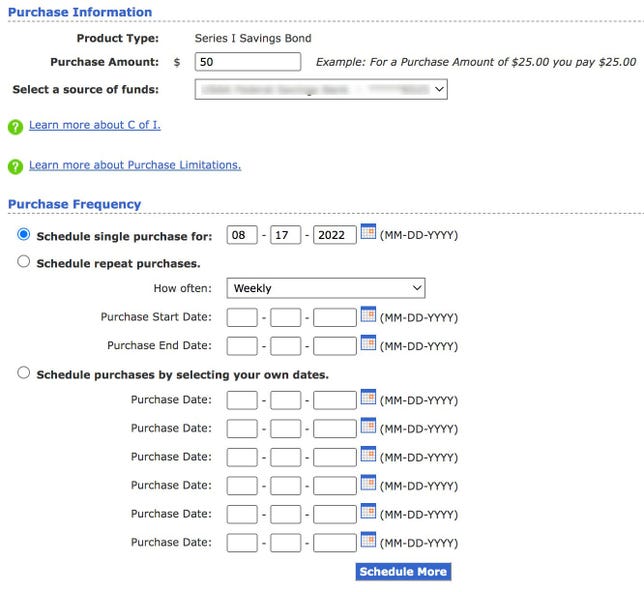

TreasuryDirect.gov allows you to make a one-time purchase or recurring purchase I bonds.

TreasuryDirect.gov/Screenshot by Peter Butler

Variable rates on I bonds represent the inflation rate for the past year. It is the rate at which you will earn interest on your savings for the first six month of owning an I bond. The previous record rate was determined based on a multiple the 4.81% increase of the CPI-U (which is a measure of the average price change on consumer goods for urban customers) between October 2021 & March 2022.

A profile will show you how much these bonds have paid over time. Bond price historical chartTreasuryDirect.

Get professional advice: Interest on your I-Bonds is paid at the current rate for six consecutive months, starting on the first of each month He buys they. People who bought I bonds before October 28, 2022, will receive a 9.62% interest rate until April 2023. The interest rate lag allows for you to make money for six consecutive months based upon the inflation rate several months ago.

Why you might want to buy a bond

Unless rates fall dramatically or rates on traditional deposits accounts rise sharply you will earn significantly more with I bonds than with a savings account, certificate of deposit, or savings account.

If you buy a $10,000 Bond next week at 6.89%, and that rate stays close to that level for a Year, you’ll earn approximately $689 on your savings in the first year. Even if you lose interest in the first three months and cash out a year later, you’ll still make $525.

The comparison is the The best five-year CDsIt will provide you with $350 savings on the same amount within your first year. Strong High yield savings accountYou will make about $200

I-bonds can be considered a relatively safe investment because they are backed and guaranteed by the government. They are also not as volatile than investing in the stock markets or cryptocurrency.

What are the potential risks of i bonds

If inflation drops to zero, or prices drop, your APY may drop to zero. The US experienced two six-month periods, ending in May 2009 and May 2015. These periods saw prices fall on average. The interest rate for I bonds was zero at that time.

In rare cases of deflation lasting six months, you may not earn any interest but your price will not fall below zero. This means that you will not lose money on I bonds (unless… The government is running out of itYou won’t lose any interest you owed previously.

If the Fed continues doing so raise interest ratesDeposit accounts like high-yield savings account can also have higher returns, making them more comparable with bonds. Stock gave Return double digitIt crashed in the recent years, but it also crashed in past Recession.

The downside to tying money to I bonds? You won’t have access for at least one year. You won’t be able to access your money for emergencies or purchases that are necessary. Treasury allows exemptionsFor those who have suffered from natural disasters.

Similar to the above, if you have to redeem the bond more than five years ago, the last three months’ interest will be forfeited.

Who can purchase and hold Series 1 savings bonds

Citizens of the United States (regardless about where they live), residents in the United States, civil servants of United States federal governments (regardless if you are a citizen or resident) with social protection numberYou can either purchase electronic or printed bonds.

To purchase I ebonds, you will need to create an online account. TreasuryDirectThis is only available to those 18 years old and older.

You can buy I bonds to your children or for anyone else. The bond holder is responsible for setting the $10,000 per year limit for electronic securities. Not the buyer. You can purchase I bonds to as many people as your heart desires. You can buy $40,000 per year electronically for a family of four (not including any paper bonds that you purchase with a tax refund).

I bonds can be purchased by corporations, LLCs, small business, trusts, and real-estate. Individuals can only purchase I bonds from foundations and corporations up to $10,000 per year.

How do I purchase Series 1 savings bond?

Register for an account at TreasuryDirect to get access to the following: Buy your I-BondsThe site can be used BuyDirect Property. You can cash the bonds or transfer them to your online account once they are in your account. ManageDirect page.

To purchase paper bonds, your federal tax refund must be used. shape 8888Popular business tax softwareTo indicate that you have purchased I Bonds up to $5,000. After your tax return has been processed, paper bonds will be mailed to the address you have provided.

Source link

[Denial of responsibility! reporterbyte.com is an automatic aggregator of the all world’s media. In each content, the hyperlink to the primary source is specified. All trademarks belong to their rightful owners, all materials to their authors. If you are the owner of the content and do not want us to publish your materials, please contact us by email – reporterbyte.com The content will be deleted within 24 hours.]